VINA BOOKKEEPING would like to send readers the MONTHLY NEWSLETTER IN DECEMBER 2024 (VIETNAMESE AND ENGLISH)

Details of attachments are here

VINA BOOKKEEPING would like to send readers the MONTHLY NEWSLETTER IN DECEMBER 2024 (VIETNAMESE AND ENGLISH)

Details of attachments are here

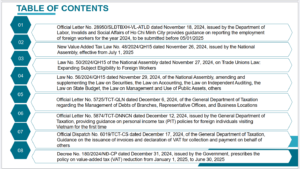

Official Letter No. 2169/TPHCM-QLDN3 issued by the Ho Chi Minh City Tax Department responds that the FDI enterprise is not eligible for tax exemption.

Official Letter No. 850/DAN-QLDN2 issued by the Da Nang Tax Department provides guidance that the subsidiary is not eligible to apply the 15% and 17% tax rates.

Thông tư số 20/2026/TT-BTC quy định chi tiết một số điều của Luật Thuế thu nhập doanh nghiệp và Nghị định số 320/2025/NĐ-CP ngày 15/12/2025 của Chính phủ

Company Registration in Vietnam How to set up a company in Vietnam VBK provides a comprehensive corporate services for your doing business in Vietnam based on our practical expertise. Whether you want to establish a business or restructure your existing operations in Vietnam, please contact us. Our team can help you in all the steps

Company Incorporation Services in Vietnam How to set up a company in Vietnam VBK provides a comprehensive corporate services for your doing business in Vietnam based on our practical expertise. Whether you want to establish a business or restructure your existing operations in Vietnam, please contact us. Our team can help you in all the

Bank Account Opening Support Service for Foreign Direct Investment (FDI) Enterprises Typically, after a business is granted the Certificate of Business Registration and the Investment Registration Certificate, FDI enterprises often need to open the following bank accounts: Direct Investment Capital Account (DICA): DICA, short for Direct Investment Capital Account, is a payment account in foreign

Corporate Secretarial & Compliance in Vietnam We provide support to businesses and other entities in corporate governance and compliance with statutory and regulatory obligations. Our assistance includes provision of specific services, such as named company secretary, authorised representative and registered office / principal place of business. Our services include the following: Board and committee meetings

Official Letter No. 218/CST-TN dated 27 January 2026 issued by the Department of Tax Policy Management and Supervision, Fees and Charges – Ministry of Finance According to the Official Letter, the Department of Tax Policy Management and Supervision, Fees and Charges provides guidance that for salary and wage payments of VND 5 million or more

The Circular provides detailed instructions on accounting vouchers, accounting accounts, bookkeeping, preparation, and presentation of financial statements for enterprises. The determination of a company’s tax obligations to the State Budget shall comply with the provisions of tax law. This Circular applies to all enterprises across various sectors and economic components. Credit institutions and branches of foreign banks shall implement the accounting regime or relevant legal documents on accounting in accordance with the guidance of the State Bank of Vietnam.

VINA BOOKKEEPING would like to send readers the MONTHLY NEWSLETTER IN DECEMBER 2025 (VIETNAMESE AND ENGLISH) Details of attachments are here

VINA BOOKKEEPING would like to send readers the MONTHLY NEWSLETTER IN FROM OCT TO NOV 2025 (VIETNAMESE AND ENGLISH) Details of attachments are here

Official Letter No. 01/TCS14-QLDN1 dated 05 January 2026 issued by Tax Sub-department 14 of Ho Chi Minh City guidance that where a company pays salaries of VND 5 million or more